Master Limited Partnerships: 2Q17 Review

2017 is shaping up to be a transition year for midstream MLPs. Domestic production of hydrocarbons has reversed trend and is once again on a growth trajectory. Crude oil production is up 910,000 barrels/day in the last 12 months and is expected to cross 10 million barrels/day of production in 2018. Demand for natural gas continues to grow driven by exports and new gas-fired electricity power plants. Natural Gas Liquids (NGLs) demand is set to spike as new petrochemical facilities begin operations. The large capital investments in  pipelines and associated infrastructure from previous years are coming on-line and hydrocarbon volumes through pipelines are set to see growth in the second half of the year. MLP price performance has been challenged so far due to a 19% decline in crude oil prices this year. The elevated correlation between crude prices and MLPs remains, but we believe this will begin to dissipate as the OPEC production cuts begin to lower global crude oil inventories in the coming months. MLPs continue to trade at a discount to historical valuation metrics. As of June, 30th 2017, Wells Fargo calculates a price to distributable cash flow (P/DCF) ratio for 2018 of 10.7x, this compares to the 5yr average P/DCF ratio of 12.9x, a 17% discount to historical levels. This discount exists despite the improved balance sheet health and renewed growth outlooks for the sector. We believe this elevated short term correlation with crude oil is presenting extremely attractive investment opportunities for long-term investors. MLP earnings are driven by volumes moving through the pipelines, not the price of the commodity. As volumes return, many MLPs will see earnings growth just by filling underutilized assets. As the market starts to recognize the strong fundamentals underlying MLPs, the crude correlation will go down. MLPs have several tailwinds that will play out in the coming months.

pipelines and associated infrastructure from previous years are coming on-line and hydrocarbon volumes through pipelines are set to see growth in the second half of the year. MLP price performance has been challenged so far due to a 19% decline in crude oil prices this year. The elevated correlation between crude prices and MLPs remains, but we believe this will begin to dissipate as the OPEC production cuts begin to lower global crude oil inventories in the coming months. MLPs continue to trade at a discount to historical valuation metrics. As of June, 30th 2017, Wells Fargo calculates a price to distributable cash flow (P/DCF) ratio for 2018 of 10.7x, this compares to the 5yr average P/DCF ratio of 12.9x, a 17% discount to historical levels. This discount exists despite the improved balance sheet health and renewed growth outlooks for the sector. We believe this elevated short term correlation with crude oil is presenting extremely attractive investment opportunities for long-term investors. MLP earnings are driven by volumes moving through the pipelines, not the price of the commodity. As volumes return, many MLPs will see earnings growth just by filling underutilized assets. As the market starts to recognize the strong fundamentals underlying MLPs, the crude correlation will go down. MLPs have several tailwinds that will play out in the coming months.

MLP Q2 Update

MLP prices were under pressure in Q2 as oil/energy sentiment turned negative due to bloated global crude inventories. The short-term volatility in crude prices does not impact most MLPs business operations and is obscuring the long-term value of the midstream sector. During the quarter, we traveled to Orlando for the MLP Association Conference where we met with management teams to get a feel for their view on their business and the sector. Many management teams expected 2017 to be a transition year as strengthening balance sheets and building distribution coverage are priorities. Many were bullish about greater utilization of their existing assets, and potential growth projects. The predominant view was MLPs will eventually break out of the high correlation with crude oil as the market sees additional data on improving fundamentals. We discussed reasons for possible weakness with fellow MLP investors at the conference. The prevailing view on weakness pointed towards the oil price correlation, low retail fund flows into the sector and too much equity issuance. The rig count, which counts the number of rigs drilling for oil and gas in the U.S has increased by over 100% in the last year. This increase is a leading indicator on volume growth, which is why we fully expect to see significant volume increases in the back half of 2017. Another tailwind for the MLP sector is the positive legislative support from the Trump Administration. Under President Obama, many pipeline projects were delayed or cancelled, Trump has reversed this and wants to capitalize on our domestic resources as we march towards energy independence. MLPs that operate in key shale basins such as the Permian and Marcellus continue to announce strong earnings and guidance surrounding growth. Permian production continues to rise and several new pipeline projects for natural gas, NGLs, and crude have been announced in recent months. The midstream industry continues to see opportunities to optimize our energy infrastructure system. Another positive for the sector, is we are entering a phase of massive new domestic energy demand from exports, petrochemical and manufacturing facilities.

Growing Demand

Volume growth is coming for natural gas, natural gas liquids (NGLs) and crude oil pipelines. Demand for natural gas continues to grow driven by LNG exports, pipeline exports to Mexico and increasing investment in natural gas-fired electricity power plants. The Energy Information Agency (EIA) projects gas-fired generating capacity to increase by 11.2 gigawatts in 2017 and 25.4 gigawatts in 2018. That is enough capacity to power over 20 million homes. Many of these new electricity plants are in the mid-Atlantic and being powered by Marcellus Shale gas. We like MLPs that deliver gas to these facilities as the contracts are typically 10-20yrs with minimum volume commitments from investment grade counterparties. We expect natural gas to play a significant role in electricity generation for decades to come as coal and nuclear plants are phased out. MLPs are playing a vital role in the buildout of infrastructure to support LNG exports. The U.S is currently exporting roughly 2 billion cubic feet (bcf) of gas from Cheniere Energy’s Sabine Pass facility. By 2021, the EIA projects exports will reach 9.2bcf as new facilities come online. MLPs actively participate in building and operating these facilities along with the pipelines that feed the facilities gas.

Another industry reaping the benefits of shale is the petrochemical industry. According to the American Chemistry Council, domestic chemical companies have invested $161B in 264 new projects since 2010. Domestic chemical manufacturing is on the verge of a renaissance due to the low-cost and abundant shale gas that has lowered feedstock prices and energy costs for chemical companies. Two of the primary natural gas liquid feedstocks being used by domestic petrochemical companies are ethane and propane. These feedstocks are processed into ethylene and propylene, both building blocks of plastics. As demand for natural gas liquids continues to grow, we wouldn’t be surprised to see chemical companies becoming joint-venture partners on associated pipeline projects. Enterprise Product Partners (EPD), the largest MLP by market cap, estimates demand for ethane is estimated to grow by 340,000 barrels/day in 2017 as petrochemical plants come on-line. Additional demand growth of 430,000 barrels/day is expected through 2020. MLPs that operate natural gas liquids pipelines and processing facilities stand to benefit from this increasing demand.

Oil Upside?

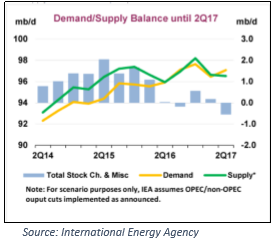

In the beginning of 2017, OPEC announced production cuts of 1.8 million barrels/day. The market rewarded OPEC by pushing the prices towards $55 per barrel as it was believed global inventory levels would begin to rapidly decline. At that point, domestic oil companies used the strength in prices to hedge their production at higher prices. Since then, oil prices have drifted to the mid $40s. The negative oil price action has been driven by two factors; rapidly increasing oil production in the U.S (good for MLPs) and global inventory levels remaining frustratingly high. We think some energy investors are failing to see the forest through the trees. Before the cuts were implemented, many OPEC countries  boosted their production so they would be able to cut production from a higher baseline. This ramp in production delayed inventory withdrawals for a few months. However, in the past month, we have seen inventory levels begin to decline at an accelerating pace. While U.S production continues to increase, the increases are not enough to offset the OPEC cuts, natural declines in oil fields and the lack of investment in new oil projects for the last 3 years. The lack of investment in new oil projects has some industry observers concerned that we could see a violent price swing to the upside as demand continues to increase and supply can’t keep up. Low oil prices continue to spur demand growth. Global oil demand is slated to increase by 1.3 million barrels/day in 2017 and an additional 1.4 million barrels/day in Source: International Energy Agency

boosted their production so they would be able to cut production from a higher baseline. This ramp in production delayed inventory withdrawals for a few months. However, in the past month, we have seen inventory levels begin to decline at an accelerating pace. While U.S production continues to increase, the increases are not enough to offset the OPEC cuts, natural declines in oil fields and the lack of investment in new oil projects for the last 3 years. The lack of investment in new oil projects has some industry observers concerned that we could see a violent price swing to the upside as demand continues to increase and supply can’t keep up. Low oil prices continue to spur demand growth. Global oil demand is slated to increase by 1.3 million barrels/day in 2017 and an additional 1.4 million barrels/day in Source: International Energy Agency

2018. That would put global demand at 99.3 million barrels/day. Much of the new demand is being driven by developing countries such as China and India. The chart above illustrates that global supply/demand balance is finally flipping towards a supply deficit. We believe the trend continues in the coming months which should push down inventories enough to see oil rally towards $50-$55 by year end.

Conclusion

With our expectation of improving energy fundamentals in the coming months, we believe MLPs have rarely been more attractive as an investment. A shift in sentiment will drive positive fund flows into the MLP sector as valuations remain very discounted versus historical levels. In recent weeks, we have seen strong insider buying, positive dividend announcements, and several new growth project announcements. MLPs continue to place multi-billion dollar projects into service, enhancing their cash flow and growth visibility. The increasing utilization of existing assets will drive earnings and distribution growth with minimal investment needed. Midstream management teams learned valuable lessons throughout the downturn which has led to better capital decisions and ultimately a stronger sector overall. The growing sources of demand for energy due to manufacturing and petrochemical companies moving back to the U.S creates demand for additional infrastructure investment. With commodity prices stabilizing and the Alerian Index yielding 7.3%, we believe MLPs offer a compelling opportunity for the long-term investor.

Best Regards,

Dave DeWitt

Bob Milnes